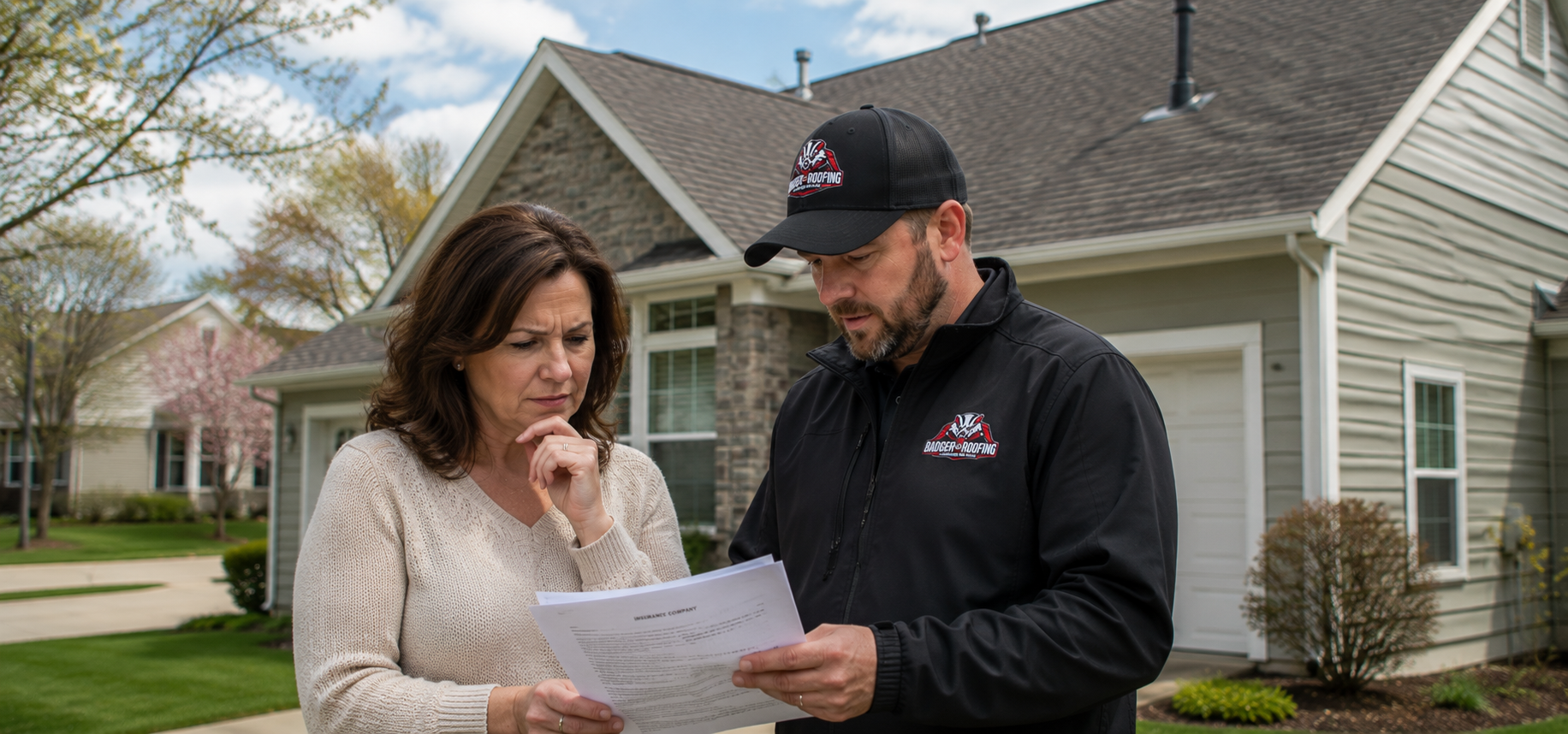

Are You Getting the Full Value Your Insurance Claim Owes You?

Most homeowners in Stoughton, McFarland, and across Dane County settle for less than their policy actually covers. They do not know how to document damage the way adjusters look for it. They do not know which line items are negotiable. They sign off on the first offer. Badger Roofing of Wisconsin handles every step of the claim process so you do not leave money on the table.

A storm rolls through Stoughton, Oregon, or Cottage Grove. Your shingles are cracked, your flashing is lifted, maybe there is hail damage you cannot even see from the ground. You file a claim. The adjuster comes out, writes a number, and leaves. That number is often the floor, not the ceiling. Without a roofing contractor who knows how insurance documentation works, you have no way to know if the scope of damage is accurate or if line items are missing.

Badger Roofing of Wisconsin works directly alongside homeowners in Stoughton, McFarland, Edgerton, and across Dane County to document every square inch of damage before your adjuster arrives, ensure the damage report reflects what is actually there, and push back when a claim is underpaid. We have done this hundreds of times. We know what adjusters look for and what they often miss. If emergency tarping is needed to stop active damage while the claim is being processed, we handle that too.

This is a separate service from our free roof inspection (before a claim is filed) and from meeting with your adjuster (one specific step we also cover in detail). Insurance Claim Help is the full picture: from the moment you suspect damage to the day repairs are complete and your insurance payout is final.

Serving Stoughton, Cottage Grove, McFarland, Oregon, Edgerton, and all of Dane County.

Five Reasons Your Insurance Claim Gets Denied, Delayed, or Underpaid

Homeowners in Stoughton, Oregon, McFarland, and across Dane County file claims every storm season and walk away with less than they are owed. Not because their policy is bad. Because no one was in their corner who knew how the process actually works.

Incomplete Damage Documentation Before the Adjuster Arrives

Adjusters are on site 30 to 45 minutes. Hail bruising, lifted flashing, soft spots on decking, and gutter damage are invisible to an untrained eye. If it is not documented before they arrive, it never makes it onto the payout report.

Supplements Left Off the Scope of Loss

Gutters, drip edge, pipe boots, ridge cap, ice and water shield, and underlayment upgrades are routinely excluded from initial adjuster reports. A contractor who knows Xactimate knows exactly which supplements to request and how to justify every line item in writing.

Depreciation Withheld and Never Recovered

Most policies release recoverable depreciation holdback only after repairs are complete and properly documented. Homeowners who skip this final step forfeit it permanently. The insurance company keeps it by default.

Storm Damage Misclassified as Wear and Tear

Insurance companies deny claims by attributing real storm damage to age or maintenance issues. A contractor who can document storm-specific damage patterns and cross-reference weather event data can challenge these classifications directly.

05 / The Biggest Mistake

No One to Push Back When the Adjuster Gets It Wrong

Once you cash or deposit the final settlement check, in most cases the claim is closed. You cannot reopen it. Homeowners who sign off before a contractor reviews the full repair cost lock themselves into a payout that may not cover the actual job. Badger Roofing of Wisconsin provides written damage assessments, photo evidence packets, and line-item reviews for homeowners in Stoughton, Edgerton, Cottage Grove, and across Dane County. We have had initial estimates revised upward by 40 to 60 percent after properly supplementing a claim.

Get Help With Your ClaimAlready Received a Claim Offer? Let Us Review It.

Badger Roofing of Wisconsin offers a free review of any insurance scope of loss for homeowners in Stoughton, Cottage Grove, McFarland, Oregon, and Edgerton. No cost, no obligation. We will tell you if the number is right.

How Badger Roofing Handles Your Insurance Claim From Start to Finish

Most contractors hand you a repair estimate and leave you to figure out the insurance side on your own. Badger Roofing of Wisconsin stays in the process at every step. From the first inspection in Stoughton to the final payout check, we know what needs to happen and we make sure it does.

Free Roof Inspection in Stoughton, WI

Before a single claim is filed, we get on your roof. We perform a complete inspection of every shingle field, valley, ridge, hip, flashing point, gutter, soffit, and penetration. We are not looking for reasons to sell you a replacement. We are building the evidence file that wins your claim. This is what separates our free roof inspection from a five-minute drive-by. Every item we find gets photographed, measured, and written up in plain language an adjuster can read.

Badger handles

- Full roof-to-gutter damage inspection at no charge

- Photo documentation of every damage point

- Written damage assessment ready before your adjuster arrives

- Weather event cross-reference to confirm storm date and hail size

Inspect

Inspect

Document Every Item Before the Adjuster Arrives

Adjusters work fast and they know what an uninformed homeowner will and will not push back on. We build your evidence packet first. Timestamped photos, measurement records, a written scope of damage, and a line-by-line list of all items your policy covers. When the adjuster walks your Cottage Grove or McFarland property, they are not seeing the damage for the first time. We are already there with documentation they cannot dismiss.

Badger handles

- Timestamped photo evidence packet organized by damage type

- Xactimate-compatible line-item damage list

- Supplement documentation for gutters, flashing, pipe boots, and decking

- Signed contractor damage statement for your claim file

Document

File the Claim and Protect Your Full Coverage

Filing a claim is not just submitting a form. The language you use, the items you list, and the order you present damage all affect the scope your adjuster opens. We walk you through every field and make sure nothing is left vague, understated, or missing. Homeowners in Stoughton and Edgerton who have filed claims on their own often discover later they described damage in a way that gave the insurance company room to minimize the payout. We close that room before you submit.

Badger handles

- Claim language review before you submit anything

- Full coverage checklist against your specific policy type

- ACV vs RCV guidance so you know what checks to expect and when

- Depreciation holdback tracking from day one

File

File

Meet With Your Adjuster With Us in Your Corner

The adjuster inspection is where most claims get decided. A homeowner alone on a roof with an adjuster has no leverage. We are on site, we have your damage file, and we walk the roof alongside the adjuster pointing out every item we documented. When the adjuster writes their scope, they know we will compare it line by line against our assessment. This step is critical enough that we built a separate page around it. You can learn exactly what happens at the adjuster meeting here. For Oregon and McFarland homeowners who have already had their adjuster visit and feel the number came in low, call us immediately. The claim can often still be supplemented.

Badger handles

- On-site presence at your adjuster inspection

- Real-time damage walkthrough with the adjuster

- Same-day scope comparison and supplement request if needed

- Pushback documentation if adjuster misclassifies storm damage as wear

Meet Adjuster

Meet Adjuster

Complete the Repair or Replacement and Close the Claim Right

Once the claim is approved we schedule and complete the repair or full replacement with our own crew. No subcontractors. No out-of-town teams. When the work is finished we help you file the completion documentation with your insurance company to release the recoverable depreciation holdback. Most homeowners in Stoughton, Edgerton, and across Dane County never collect this second check because no one told them it existed. We track it from step one and make sure you get every dollar your policy owes you.

Badger handles

- Full repair or replacement with our own Stoughton-based crew

- Completion documentation filed with your insurer

- Depreciation holdback release paperwork submitted on your behalf

- 10-year workmanship warranty on every job we complete

Repair or Replace

Repair or Replace

Ready to start the process? Call Badger Roofing of Wisconsin today.

Your Policy Covers More Than the Adjuster Told You

Most homeowners in Stoughton and across Dane County accept the first number they are given. Badger Roofing of Wisconsin reviews every scope of loss at no charge. If your claim was underpaid, we will tell you and we will fight to fix it.

Completed

insured storm claims

Why Stoughton Homeowners Trust Badger Roofing With Their Insurance Claims

Any contractor can hand you an estimate. Very few know how to fight for the full value of your claim. Badger Roofing of Wisconsin has been doing this for over 10 years in Stoughton, Cottage Grove, McFarland, and across Dane County. We stay in the process from inspection to final payout.

We Document Before Your Adjuster Arrives

We build your full evidence file first. Timestamped photos, written damage scope, and supplement lists are ready before the adjuster sets foot on your property.

We Know What Adjusters Miss

Hail bruising, lifted flashing, soft decking, and missing supplement line items are invisible to an untrained eye. We find them and make sure they make it onto your payout.

We Fight Underpaid Claims

When the first offer comes in low, we provide written pushback with documentation. We have had initial estimates revised upward by 40 to 60 percent after supplementing a claim.

We Handle the Process So You Do Not Have To

From the first inspection call to the final depreciation holdback check, we manage every step. You should not have to become an insurance expert to get what your policy owes you.

Stoughton-Based, Not a Storm Chaser

We are based in Stoughton, WI and have been for over 10 years. We are not a crew that follows storm events from out of state. We are your neighbors and we are here year-round.

10-Year Workmanship Warranty

Every repair and replacement Badger Roofing of Wisconsin completes is backed by our 10-year workmanship warranty. We stand behind the work long after the claim is closed.

Your Insurance Claim Questions Answered

Straight answers about the insurance claim process, supplements, depreciation holdbacks, and your rights as a homeowner in Stoughton, Dane County, and across Rock County.

Need help with a claim?

Free claim review, no obligation, no pressure. Call (608) 575-3416 Monday to Saturday, 7:00 AM to 7:00 PMACV stands for Actual Cash Value and RCV stands for Replacement Cost Value. ACV is the depreciated value of your roof at the time of the loss, factoring in age and wear. RCV is the full cost to replace the roof with new materials at current prices.

Most standard Wisconsin homeowners policies pay ACV first, then release a second check called the recoverable depreciation holdback once you complete the repairs and submit documentation. The gap between these two numbers is often thousands of dollars. Homeowners who do not know to file for the holdback release after repairs are finished forfeit it permanently. Badger Roofing of Wisconsin tracks this from the first inspection and makes sure you collect both checks.

In most cases, no. Once you cash or deposit the final settlement check, the claim is considered closed under most Wisconsin homeowners insurance policies. Reopening it for additional damage found after the fact is extremely difficult and usually requires proving the damage was hidden and not discoverable at the time of the original inspection.

This is exactly why documentation before you accept any offer is critical. If you have already received a settlement offer but have not yet cashed the final check, call us immediately. There is often still time to supplement the claim with additional documentation and request a revised scope from your insurer. We review existing claim offers at no charge for homeowners across Stoughton and Dane County.

Supplementing a claim means submitting additional documentation to your insurance company after the initial adjuster scope has been written, requesting that specific line items be added or adjusted. Common supplements include gutters, drip edge, pipe boot replacements, ice and water shield upgrades, additional decking, and code-required improvements that adjusters routinely leave off the initial estimate.

A contractor who knows how to read and write an Xactimate estimate can identify every missing line item and submit a written supplement request with supporting documentation. We have had initial insurance estimates revised upward by 40 to 60 percent through the supplement process for homeowners in Stoughton, Cottage Grove, and McFarland. Supplementing is not fraudulent. It is holding the insurance company to the full scope of what your policy covers.

You are not required to have a contractor present, but it is strongly in your interest. An adjuster working alone with a homeowner on site writes a scope based entirely on what they observe and choose to include. A contractor who is also on the roof with a documented damage file can point out specific damage items in real time, reference the pre-built evidence packet, and flag discrepancies on the spot if the adjuster misses or minimizes anything.

Adjusters know that experienced contractors are watching the scope in real time and the claims we manage for homeowners in Stoughton, Oregon, and Edgerton consistently produce higher initial payouts than claims where homeowners met the adjuster without representation. We attend the adjuster inspection as part of our standard claim process at no additional charge.

A denial is not necessarily final. Wisconsin homeowners have the right to appeal a denied claim by submitting additional documentation, requesting a re-inspection, or invoking the appraisal clause in their policy. The appraisal process allows each party to hire an independent appraiser who then agrees on a neutral umpire to settle disputed damage amounts.

Before appealing, you need a contractor-prepared damage report that specifically addresses the reason for denial. Most often this is a wear and tear misclassification or a determination that the damage does not meet the insurer's functional damage threshold. We review denied claim documentation at no charge for homeowners in Stoughton, McFarland, Cottage Grove, and across Dane County and tell you honestly whether an appeal is worth pursuing and what documentation you need to support it.

From first inspection to final payout, a straightforward claim typically takes 4 to 8 weeks. The timeline breaks down roughly as follows: contractor inspection and documentation takes 1 to 3 days, adjuster scheduling and visit typically takes 1 to 2 weeks after you file, the initial claim decision from your insurer is required within 30 days under Wisconsin insurance law, and supplement requests add 1 to 2 weeks if needed.

The depreciation holdback release after repairs are completed adds another 1 to 2 weeks on top of that. Claims that involve denied items, underpayment disputes, or supplement negotiations run longer. The single fastest way to move through the process is to have complete documentation ready before the adjuster arrives. That is exactly what Badger Roofing of Wisconsin builds for every homeowner we work with in Stoughton and across Dane County.